Ever picked up your prescription and been shocked that your generic drug cost more than the brand-name version? You’re not alone. Millions of people in the U.S. face this exact situation every month-and most have no idea why. It’s not a mistake. It’s not fraud. It’s the result of a system called tiered copays, and it’s designed to make you pay more for some generics-even when they’re chemically identical to cheaper ones.

How Tiered Copays Actually Work

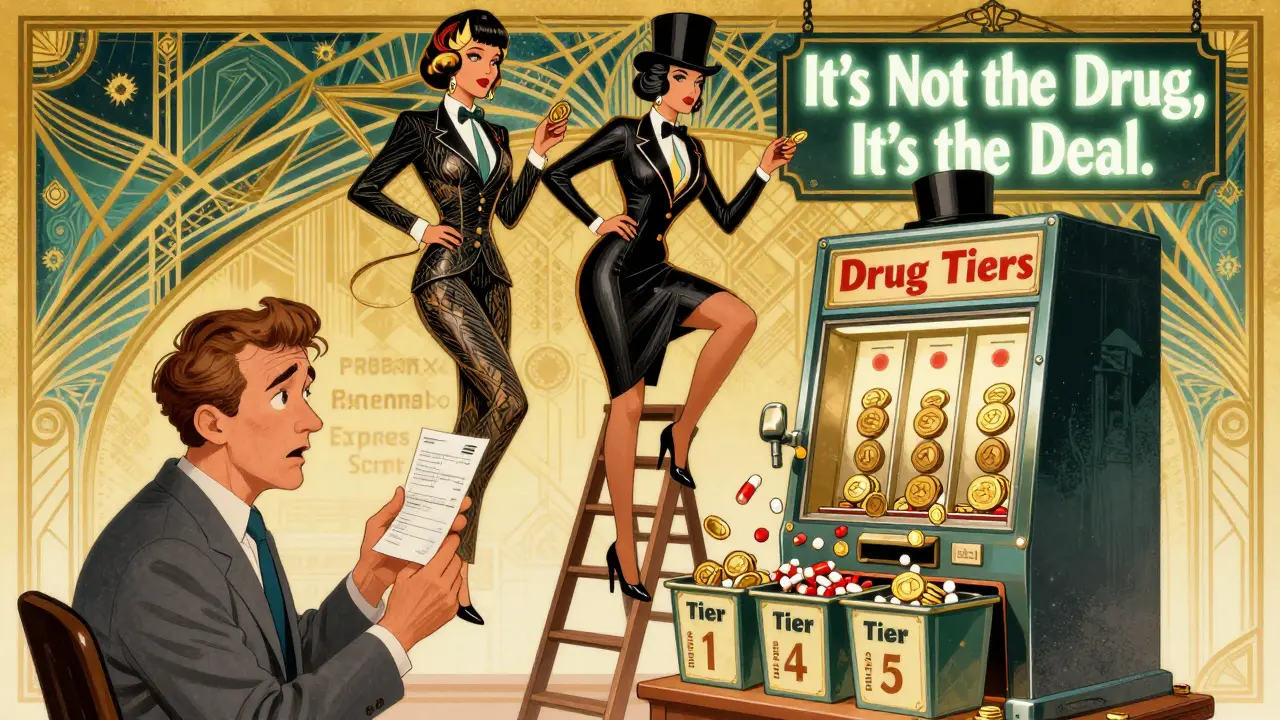

Most health plans don’t charge the same amount for every drug. Instead, they sort medications into tiers, like levels in a video game. Each tier has its own price tag. Tier 1 is the cheapest. Tier 5 is the most expensive. The idea sounds simple: encourage people to pick lower-cost drugs. But here’s where it gets messy.- Tier 1: Preferred generics. Usually $0-$15 for a 30-day supply.

- Tier 2: Preferred brand-name drugs. Around $25-$50.

- Tier 3: Non-preferred brand-name drugs. $60-$100.

- Tier 4: Preferred specialty drugs. You pay 20-25% of the cost.

- Tier 5: Non-preferred specialty drugs. You pay 30-40%.

Why Your Generic Is in a Higher Tier

You might think: "If it’s the same chemical, why is it more expensive?" The answer is simple: it’s not about the drug. It’s about the deal. Pharmacy Benefit Managers-companies like CVS Caremark, Express Scripts, and OptumRx-negotiate discounts with drug manufacturers. The bigger the discount, the lower the tier the drug gets. If your generic levothyroxine is in Tier 3 instead of Tier 1, it’s not because it’s less effective. It’s because the manufacturer of your version didn’t offer a big enough rebate to the PBM. Dr. Dennis G. Smith, former director of the Center for Medicaid and CHIP Services, put it bluntly: "Preferred status has nothing to do with clinical superiority-it’s entirely about the rebates and discounts PBMs negotiate with manufacturers." This means two identical pills-one made by Company A, one by Company B-can cost you $5 vs. $45. The only difference? The contract between the PBM and the manufacturer.

The Real Cost of "Generic" Confusion

Patients are often blindsided by this. A 2023 survey by the Patient Advocate Foundation found that 41% of insured adults had experienced a generic drug suddenly costing more than expected. And 68% of them couldn’t get a clear explanation from their insurer. One Reddit user, "PharmaPatient87," described getting their levothyroxine refill and seeing a $45 copay-up from $5. Their doctor confirmed all generics are the same. But the insurer wouldn’t say why the price jumped. That’s not unusual. Worse, pharmacists are sometimes allowed to swap your prescription for a "preferred" generic without telling you. This is called a therapeutic interchange. It might save money for the plan, but if you’ve been stable on one generic for years, switching-even to another "identical" version-can cause side effects or worsen symptoms. Studies show that when diabetes meds moved from Tier 2 to Tier 3, adherence dropped by 7.3%.How to Fight Back

You don’t have to accept this. There are real ways to reduce your costs.- Check your plan’s formulary. Every year, around October, Medicare and many employer plans update their drug lists. Download the latest version. Look up your medication by name-not just the brand, but the generic too.

- Ask your pharmacist. Say: "Is there a preferred generic version of this drug?" They can often switch you to a cheaper one without calling your doctor.

- Use tools like GoodRx or SmithRx. These apps show you the cash price and the copay across different tiers. Sometimes paying cash is cheaper than using your insurance.

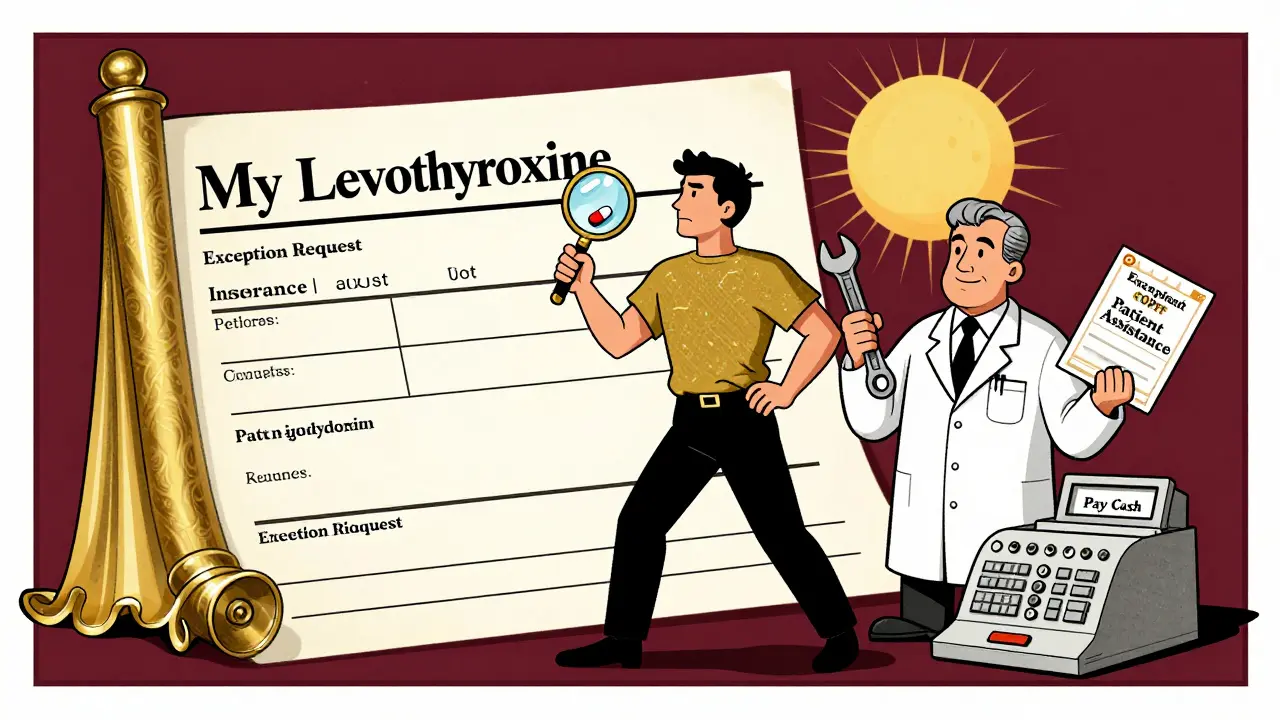

- Request an exception. If your drug moved to a higher tier, you can file a formal appeal. Your doctor can submit a letter saying the drug is medically necessary. Success rate? About 63%.

- Look for manufacturer coupons. Many drugmakers offer patient assistance programs. In 2023, these programs covered 22% of specialty drug costs for eligible patients.

What’s Changing in 2025 and Beyond

The system isn’t going away-but it’s under pressure. Starting in 2025, Medicare will cap out-of-pocket drug costs at $2,000 per year. That’s a big win. But it doesn’t change how drugs are tiered. It just limits how much you pay in total. Meanwhile, PBMs are making new moves. UnitedHealthcare moved popular generics like atorvastatin and lisinopril to $0 copays in 2024. But they also moved 87 other generics to higher tiers because their rebates expired. Express Scripts did the same. The future? Fewer tiers. Experts predict the average plan will drop from five tiers to four by 2026. But the core problem will remain: drug pricing is controlled by contracts, not clinical need.What You Need to Remember

- A generic drug isn’t always the cheapest option on your plan. - The difference in price has nothing to do with quality or effectiveness. - Your insurer doesn’t have to explain why a drug is in a higher tier. - You have rights: you can ask for a different version, file an appeal, or pay cash. If your generic costs more than expected, it’s not your fault. It’s the system. But you’re not powerless. Know your options. Ask questions. Push back. And don’t assume your pharmacy’s first choice is your best choice.Why is my generic drug more expensive than the brand-name one?

It’s not about the drug-it’s about the contract. Your insurance plan’s Pharmacy Benefit Manager (PBM) negotiates rebates with drug manufacturers. If the maker of your generic didn’t offer a big enough discount, the PBM places it in a higher tier with a higher copay-even if it’s chemically identical to a cheaper version. The brand-name drug might be in a lower tier because its manufacturer pays a larger rebate.

Are all generic drugs the same?

Yes, legally. All generic drugs must meet the same FDA standards as brand-name drugs: same active ingredient, strength, dosage, and effectiveness. But insurers may still place different generic brands into different tiers based on which manufacturer gave them the best rebate. That’s why two identical pills can cost you $5 vs. $45.

Can my pharmacist switch my generic without telling me?

Yes, in many cases. This is called a therapeutic interchange. Pharmacists can substitute a "preferred" generic for the one your doctor prescribed, unless your doctor wrote "dispense as written" on the prescription. If you’re stable on a specific generic, ask your doctor to block substitutions or request the exact brand you’re used to.

How do I find out which tier my drug is on?

Log in to your insurer’s website and look for the formulary or drug list. It’s usually updated every October. You can also call customer service and ask for the tier level of your specific generic drug by name. Third-party tools like GoodRx and SmithRx also show tier information and cash prices.

What if my drug moved to a higher tier mid-year?

You can file an exception request. Ask your doctor to write a letter explaining why you need that specific drug-for example, if switching caused side effects or reduced effectiveness. Submit it to your insurer. About 63% of these requests are approved. You can also check if the manufacturer offers a coupon or patient assistance program to cover the difference.

Will the new $2,000 Medicare cap change tiered copays?

No. The $2,000 out-of-pocket cap for Medicare Part D in 2025 limits how much you pay in total-but it doesn’t change how drugs are grouped into tiers. Your generic might still be in Tier 3, and you’ll still pay more for it than a Tier 1 drug. The cap just stops you from paying more than $2,000 total for all your drugs in a year.

I had no idea generics could be in different tiers. My levothyroxine jumped from $5 to $42 last month and my pharmacist just shrugged. I thought it was a glitch. Now I get it - it’s not about the pill, it’s about who paid the PBM the most. This system is wild.

so basically pharma companies are playing monopoly with our health? lol. if two pills are chemically same why do we even have tiers? it’s like buying milk and paying more because the cow was painted blue. capitalism is a joke.

This is so frustrating but also so important to talk about. I’ve had friends who skipped doses because they couldn’t afford the surprise copay. We need to push back - not just individually but as a community. Maybe we can start a local group to help people navigate formularies? I’d join.

THEY’RE LYING TO US. EVERY SINGLE DAY. PBMs are crooks. They don’t care if you have seizures from switching generics. They care about their quarterly bonuses. I’m done being a pawn in this scam. I’m filing an exception next week and I’m telling everyone I know.

I just checked my formulary and my lisinopril is tier 3 now. I’ve been on it for 7 years. No one told me. My doctor didn’t know. The pharmacy didn’t say anything. I’m just supposed to notice the price jump and not ask why. This is insane

OMG YES 😭 I just cried at the pharmacy when my generic albuterol went from $10 to $55. I thought I was going crazy. GoodRx saved me - cash price was $12. I’m never using insurance for generics again. 🙏💊 #PharmaScam

While the system is undeniably flawed, it’s worth noting that PBMs do provide administrative infrastructure that allows insurers to manage drug benefits at scale. The real issue lies in the lack of transparency and accountability. A regulatory framework that mandates disclosure of rebate structures might be more effective than outright elimination of tiering.

People don’t realize this is deliberate. PBMs are owned by insurance giants. They want you to pay more so they can jack up premiums later. And your doctor? They’re paid by pharma reps to push certain brands. You think this is about health? It’s about profit. Wake up.

I’ve been researching this for a year. The tier system exists because PBMs are incentivized to steer patients toward drugs that give them kickbacks - not toward what’s clinically optimal. The FDA doesn’t regulate pricing. Congress doesn’t regulate PBMs. So the burden falls on patients to become drug pricing detectives. That’s not healthcare - that’s survival.

Just spoke to my insurer. They said they can’t disclose rebate amounts because it’s "proprietary." So I can’t even argue why my drug is in tier 4. Sounds like a black box designed to confuse people into giving up. I’m using GoodRx now.

They’re all in on it. CVS Caremark, Optum, Express Scripts - they’re all owned by big health conglomerates. The brand-name drugs are just there to make you think you have options. The real money’s in the generics nobody knows about. And guess what? Your doctor gets a cut if they prescribe the "preferred" one. Wake up.

I’ve been on the same generic for 12 years and last month my copay tripled. I called my insurance, they said "it’s on the formulary list" - but didn’t say why. I called my doctor, they said "oh yeah, that happened to me too" and handed me a sample of the brand-name version. No explanation. No apology. Just a freebie. Meanwhile my rent went up, my car broke down, and now I’m choosing between insulin and groceries. This isn’t a system. It’s a trap.

Thank you for writing this. I’ve seen so many people suffer silently because they don’t know how to fight back. Your tips are practical and clear. I’m sharing this with my senior group next week. We need more voices like yours - calm, factual, and relentless.